E-commerce Returns, Return Collection, Secondary Market, B2B Liquidation, Business Model Innovation, Re-commerce, Generative AI

Transforming E-commerce Returns: Rethinking Challenges for a Sustainable Future

How Retailers and E-Commerce Brands Currently Handle Product Return Collection and Resale, and What Lies Ahead

[Note]: As a marketplace evangelist with experience in the secondary market and e-commerce post-purchase landscape, I aim to share my insights and outline a viable path forward for handling e-commerce returns. I advocate for business model innovations that make managing returns cost-effective and efficient for brands and consumers alike. It’s time for both e-commerce leaders and shoppers to rethink returns, moving away from viewing them negatively to seeing them as an unavoidable part of online shopping that can be managed more effectively. By shifting our perspective, we have an opportunity to create a more sustainable approach to dealing with unwanted and returned items, offering financial benefits for all involved, reducing waste, and giving these often high-quality items a second chance. This collaborative effort can lead to better economics for e-commerce returns, encouraging brands to support a more sustainable e-commerce future.

Introduction

The pandemic-induced boom in online shopping and e-commerce saw sales soar to an impressive $1.2 trillion between 2022 and 2023 [Chart 1], highlighting a remarkable shift in consumer behavior. However, this shift came with its challenges, primarily due to more lenient return policies and the inherent limitations of online shopping, such as the inability to physically inspect products before purchase.

Consequently, this led to a significant uptick in the e-commerce return rate, culminating in approximately $816.8 billion worth of goods returned across both online and brick-and-mortar sales — a figure that continues to grow year over year. Jonathan Poma, CEO of Loop Returns, underscored this trend in a recent Yahoo Finance interview, noting a 35% increase in total return volume on December 26, 2023, compared to the previous year.

The surge in returns has notably impacted retailers and online brands, eroding profits through added costs associated with reverse logistics, including transportation, warehousing, sorting, and grading of returned items. The situation is compounded when items become out-of-season and must be resold at a discount or disposed of at a loss, further diminishing the bottom line.

Returns can be costly for retailers. According to Reuters, the typical return costs retailers about $30. In response, many retailers have begun reevaluating their return policies to mitigate these costs. Tactics have included shortening refund windows, introducing restocking fees, and modifying policies to offer store credit, deem some items returnless, or directly charge for returns, especially in high-return categories like clothing. This shift in strategy is evident, with an estimated 44% of retailers (e.g., American Eagle, J.Crew, Saks Fifth Avenue, H&M, Zara) now imposing a fee for processing returns, a significant increase from 33% in 2021 [source: Narvar].

Amid these industry shifts, a critical challenge remains: the lack of centralized accountability in managing returns and a comprehensive understanding of the economics behind them, as highlighted by McKinsey’s report on improving returns management for apparel companies. This oversight often relegates returns to mere post-purchase afterthoughts, overlooking potential opportunities for revenue optimization. McKinsey’s recommendation advocates for a strategic reorientation towards centralizing return management, suggesting the appointment of a dedicated senior leader to oversee and streamline return processes. This alignment would improve efficiency and integrate return management with broader business objectives, such as enhancing product return rates and supporting sustainable business practices. Such a holistic approach aims to elevate the management of returns from its traditional limitations of reverse logistics to a strategic component of enhancing customer loyalty and driving top-line growth.

How big is the e-commerce return economy, and why is it happening?

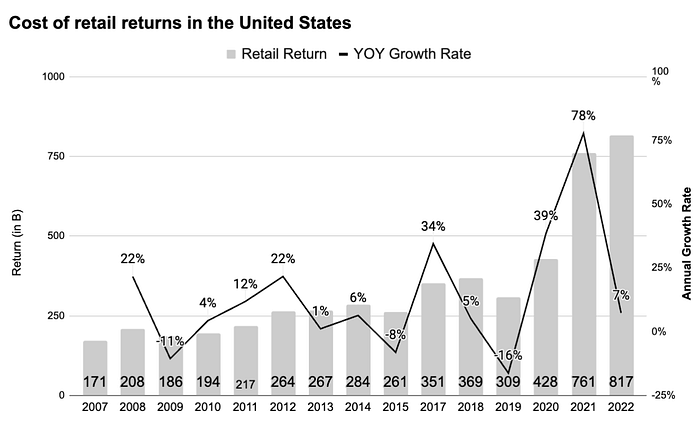

In 2022, the rate of returns nearly doubled compared to pre-pandemic figures, reaching 16.5% of total U.S. retail sales, which equates to $816.8 billion worth of goods, as reported by the National Retail Federation (NRF) [Chart 2]. The pandemic significantly accelerated retailers’ shift towards e-commerce, a move that saw product returns jump from $70 billion in 2019 to $213 billion in 2022, according to Statista. It’s noted that online sales tend to see a higher incidence of returns, with e-commerce return rates averaging 30%, in stark contrast to the 10% typically seen in physical store sales.

Furthermore, in the U.S. alone, the carbon footprint associated with shipping returns in 2022 was around 24 million metric tons of CO2, which is 50% higher than the figures recorded during the e-commerce surge in 2020.

The dramatic increase in the retail return rate from 2019 to the present can be attributed to various factors, which vary by product category and business model. Below, we explore some of the key reasons behind this unprecedented growth in retail returns:

Generous Return Policies: Balancing Online Shopping Confidence with the Challenge of Increased Returns

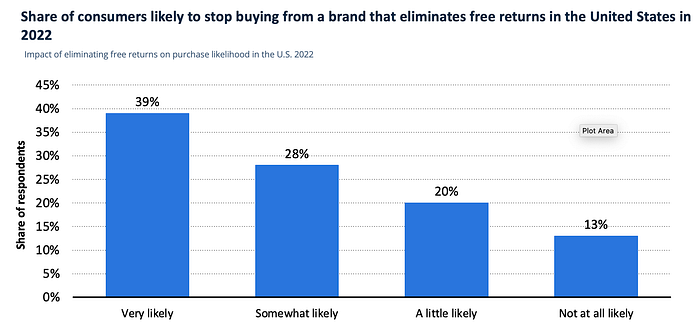

The impact of return policies on consumer purchasing behavior is profound. A significant majority (81%) of shoppers consider free shipping crucial for online purchases. Moreover, 87% of consumers are somewhat likely to discontinue shopping with a brand that ceases to offer free returns, with 39% stating they are very likely to do so. Chart 3 underscores the critical role of consumer-friendly policies like free returns in driving sales and fostering customer loyalty.

“84% of customers would not return to a retailer after a bad returns experience” (Data source: Klama)

Prioritizing Growth over Sustainable profitability at all Costs

The pandemic saw e-commerce, especially apparel, prioritizing growth, sometimes at the expense of profitability. This strategy, propelled by online shopping convenience and pandemic restrictions, led to increased sales and return rates, thereby impacting profitability. The underlying strategy resembled Clayton Christensen’s concept of prioritizing growth (“bad money”) over sustainable profitability (“good money”). As companies offered extensive promotions and advertisements to boost sales, they often overlooked the significant costs associated with returns. This growth-first mentality, typical in the early-stage and venture capital community, has shifted towards emphasizing profitability.

The “Buy Now, Pay Later” (BNPL) Effect: Fueling Impulse Purchases

Since the pandemic, the popularity of BNPL services like Klarna, Afterpay, Affirm, and PayPal has surged, especially in the United States, where BNPL payments were expected to grow by 66.5% in 2022, reaching an estimated $443 billion by 2028. This growth, fueled by the convenience and flexibility of BNPL options, allows consumers to make purchases without immediate financial pressure and be more impulsive, which could lead to higher returns. This trend, prevalent among Gen X and millennial shoppers for managing cash flow, also presents challenges for e-commerce, potentially contributing to increased purchasing and higher return rates.

Lack of Investment In Accurate Product Descriptions

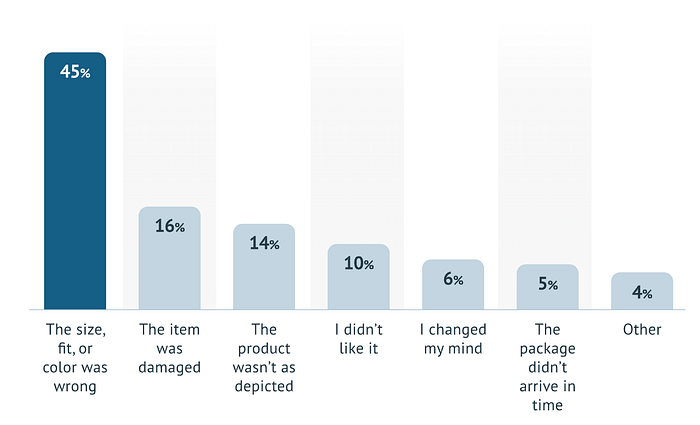

Investing in detailed and accurate product descriptions is key to reducing returns. American consumers average about eight returns yearly, with sizing, fit, and color being the primary reasons. According to Narvar’s 2022 State of Returns, “sizing, fit, and color” is the top cause for all retail returns, accounting for 45% of returns in 2022 [Chart 4].

Clear instructions, model sizes, and material details in online fashion stores can significantly lower returns. Employing advanced technologies like AI and machine learning for analyzing customer feedback and AR and VR for realistic product previews can bridge the gap between digital representation and the actual product. While the full impact of technology adoption on reducing returns is yet to be determined, it’s a promising area for improving customer experience and finding products more efficiently and confidently.

The final word here is that returns have become an inevitable component of e-commerce. Despite efforts to optimize return logistics and promote more sustainable consumer behavior, return rates are expected to remain stable or increase. Attempts to reduce returns through stricter policies or improved product descriptions, while helpful, may not fundamentally change return rates, indicating a need for innovative approaches and non-linear solutions beyond conventional strategies (or, for instance, encouraging consumers to buy less).

Buying less won’t fix the product return as quickly as adopting new habits to return unwanted items.

In essence, the complexity of the problem required the need for newer business model innovation beyond traditional ones, aligning with Professor Thales’ decoupling theory. His theory highlights how consumer behavior, rather than company actions, often drives market disruption. A sustainable solution necessitates reevaluating the entire consumer return value chain, aiming to eliminate or reinvent activities that erode value. This could lead to a more cost-effective and convenient system for all stakeholders involved. The upcoming sections will delve deeper into these innovative strategies.

Managing Online Return Costs and the Fate of E-commerce Returns

Key Drivers of Return Costs

The main associated cost to handle returns encompasses several factors that significantly impact the financial aspect of e-commerce operations. Shipping, warehousing, and labor are among the primary contributors to the high costs associated with returns. Receiving, inspecting, and restocking returned items can be time-consuming and resource-intensive, leading to additional expenses for retailers. Moreover, the timing of returns can also pose challenges for retailers.

Many returned items often come back out of season, making it difficult to resell them at their original price. To recover some value from these out-of-season items, retailers may also need to sell them at hefty markdowns, further reducing profits. [Chart 5] outlines the components of reverse logistics costs and various immediate disposition strategies for handling returns, ranging from liquidation to disposal and landfill.

Economic Impact of Returns

According to Reverse logistics company Optoro, the cost of processing return could be, on average, up to 66% of its sale price, depending on categories (e.g., high-value electronics, such as laptops, tablets, and cell phones will see the highest reverse logistics costs in terms of total dollar cost per unit) when accounting for all costs of reverse logistics, discount loss, and liquidation. [Chart 6] will have the breakdown of this 66% (e.g., average $33 in processing fee or 66% value of a $50 product).

Strategies to Mitigate Return Costs

With the rise in e-commerce costs and challenging unit economics, some retailers have adopted “returnless refunds,” letting customers keep products while still issuing refunds, avoiding additional costs. Narvar reports that 75% of consumers have received refunds without returning the product.

Additionally, while many companies have traditionally offered free return shipping to enhance customer satisfaction, there’s a shift in this trend due to high reverse logistics costs. More retailers like Amazon, H&M, J. Crew, and Zara are beginning to impose return fees, with Amazon charging $1 at non-preferred locations. This change indicates a move towards sharing return costs, especially for non-loyal customers, and reflects the significant impact of transportation and inbound shipping expenses on the economics of returns. This approach may also incentivize customers to be more thoughtful in their purchases and help offset the costs associated with return logistics.

Among some of the other tactics to mitigate the high cost of returns, retailers like Wayfair and Amazon may offer discounts to entice customers to keep the items they purchased (often called “discount to keep”). Retailers may offer customers discounts to keep some qualified items with high returns (e.g., furniture) or very low values (e.g., a $7 T-shirt from Walmart ) rather than returning them. While mitigating immediate costs, this strategy may not be a sustainable long-term solution due to potential system abuse and varied reasons for returns.

Final Destinations for online returns

The journey of product returns via reverse logistics involves several steps and disposition routes. Products returned by customers are first collected and transported back to a warehouse or processing center. Here, they undergo an assessment to determine their condition and the most suitable next step. This could include refurbishment, B2B/B2C resale, recycling, donation, or, in some cases, disposal. The disposition decision often depends on factors like the product’s condition, cost-effectiveness of refurbishment, potential resale value, and brand image considerations. According to Optoro, it’s estimated that 25% of returned products are disposed of and made in landfills.

Many retailers end up throwing away over 25 percent of their returns. Holistically, that ends up being over 5 billion pounds of goods that end up in landfills a year from returns (Tobin Moore, former CEO of Optoro)

According to CNBC, Amazon offers four return disposition options to its third-party sellers: (a) Return to the seller ($0.52+ cost per unit), (b) bulk liquidation ($0.25+ cost per unit +15% referral fee), (c) Grade and resell by Amazon ($1.5+ cost per unit), and (d) disposal ($0.52+ cost per unit), among which disposal can be up to 33% cheaper than grading /reselling them by Amazon. As a result, unfortunately, many online sellers opt for disposal and landfill as an economical method when they DO NOT have in-house return processing capabilities or choose to avoid working with third-party bulk liquidation companies and auction marketplaces (e.g., Bstock.com, liquidation.com, etc.) due to the minimum recovery rates (~5–8 cents recovery for each dollar of return), limited visibility into the aftermarket and or brand image protection.

The rising trend towards disposal and landfills is noteworthy and concerning and is not only offered by Amazon. Even some luxury brands may prioritize brand protection over economic efficiency and sustainability by destroying their high-end products. Instances like Burberry or Cartier burning premium items exemplify the luxury sector’s delicate balance between cost management and maintaining brand exclusivity.

Despite the challenges, there is potential for e-commerce brands to benefit from grading and reselling unwanted/returned items within a circular economy, a strategy that reduces waste and loss. Around 80%–85% of unwanted products are OK and sellable on average [Chart 4]. However, the reality is more complex. High costs associated with reverse logistics and the challenges of rapidly reselling returned goods complicate this process. Furthermore, even when brands effectively process returns for resale in secondary markets, finding buyers willing to pay premium prices, particularly on a large scale and on time, is daunting.

The following sections will delve deeper into the reverse logistics journey and explore strategies for managing returned products effectively. In exploring these dynamics, we aim to dissect the consumer value chain and the economics of returns, offering insights into both current practices and innovative solutions for managing e-commerce returns.

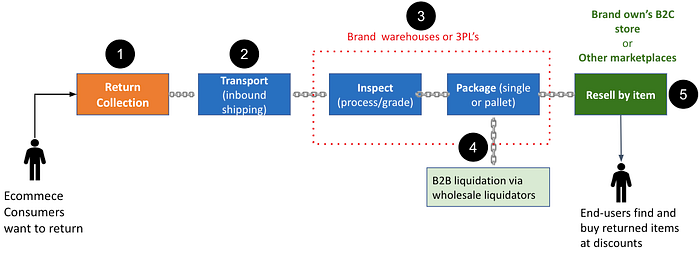

Chart 7 outlines the process and components necessary for reselling a returned item, highlighting the critical stages from initial return to resale (note: Stages 4 and 5 are either or).

The Spectrum of Solutions for Product Return Collection

A National Retail Federation study highlights that 70% of online shoppers prioritize retailers with easy return policies, indicating that a smooth and hassle-free return experience, from collecting the items through refunding and post-return, can significantly boost customer loyalty and can steal future retention.

The initial stages of return collection and transportation are crucial touchpoints that influence customer return satisfaction and retention [Chart 7]. Entrepreneurs are increasingly focusing on innovative return collection methods to offer convenience while improving retailers' cost-efficiency. These methods range from traditional drop-offs at postal services to doorstep pickups and even newer, tech-driven solutions like box-free returns at local drop-off points such as malls or partner stores.

Chart 8 briefly outlines various widespread methods employed globally to collect returned products, differing in their convenience levels for customers (returners) and cost structures for brands. These solutions vary from traditional package drop-off at the brands’ stores/postal couriers to picking up the items from the customer’s door.

As E-commerce and return rates grow, brands and emerging entrepreneurs continue experimenting with fresh concepts, although some might only sometimes yield sustainable economic models. In particular, some emerging startups focus on enhancing convenience in the return process by picking up items from customers’ doorsteps, regardless of the original packaging. An early example from 2015 is the hype and well-funded company Shyp, which aimed, among the first ones, to address the challenge of collecting E-commerce returns directly from customers’ homes (among other on-demand delivery services). However, Shyp ceased operations in 2018. The main reason, as noted by TechCrunch, was their initial offering of a $5 flat fee for pickup and packaging, irrespective of the item’s size or weight. This pricing structure proved appealing to customers but posed profitability challenges for Shyp. Since most individuals only ship items occasionally, the demand for Shyp’s service fell short of the company’s expectations.

Much evidence has yet to support that standalone product return pickup services will likely prevail in the long term due to low demand (Chart 9 reports that only 13% of customers preferred the return pick up from their doorsteps) and high operating costs. The closure of Shyp, an on-demand shipping company, is a sign of the challenges facing these businesses. On-demand shipping companies face increased costs for couriers, packaging, and shipping. They also face competition from traditional shipping companies with lower costs and a more comprehensive network of delivery locations (e.g., UPS, DHL).

To diversify their delivery services and enhance the economics of their on-demand offerings, DoorDash and Uber also introduced a product return pickup service, charging a flat fee of $3–$5. This service, available in select cities, aimed to simplify the return process for customers by offering a convenient and seamless experience. Although Uber’s services were later discontinued, it’s too soon to determine their success in the product return sector. However, given the rising trend in e-commerce returns and the increasing consumer demand for a hassle-free first-mile return collection, it’s likely that the market will continue to attract new startups and investments, exploring innovative business models in this space.

I believe that first-mile return collection is as crucial in reverse logistics as last-mile delivery is in traditional logistics. It marks the beginning of the reverse logistics journey by retrieving returned items from customers, influencing customer satisfaction through its cost and convenience while also impacting retailers’ operational efficiency and potential cost savings.

Shifting from the growing trend of return pickups to drop-offs, which remains the preferred return method in the U.S. [Chart 9], customers are inclined to return packages at nationwide locations of mail carriers like USPS, UPS, and DHL or selected third-party sites. This shift has seen major online retailers like Amazon partnering with retail stores such as Kohl’s and Staples, establishing more return hubs to streamline the process and improve return logistics economically. Through this model, Amazon achieves economies of scale by aggregating returns for bulk transportation to their processing centers rather than handling returns individually. This approach also places the initial responsibility of the first mile of return collection on customers, who bear the cost of time and effort to reach these drop-off points. Conversely, retail partners like Kohl’s and Staples gain from increased store visits and potential additional purchases made by Amazon customers returning items, enhancing overall store traffic and sales.

As some new innovators in the return collection landscape [Chart 8], tech companies such as Happy Returns have played a crucial role in enhancing the return experience for customers and simplifying the process for e-commerce brands. Established in the US in 2015 and later becoming part of PayPal in 2021 before being acquired by UPS in 2023, Happy Returns introduced “Return Bars” located in shopping centers, where customers can return items seamlessly without needing a box or shipping label. In Canada, similar initiatives like ReturnBear are gaining traction. These services are particularly valuable for e-commerce entities and online retailers without physical stores, helping them refine their return processes. This model significantly improves convenience for customers and streamlines the return process, making it more efficient and economically favorable.

Last but not least, Walmart, Target, and Nordstrom are leading the charge with a novel “Curbside Return” initiative designed to make the return process more convenient for their customers. This service lets customers easily return items directly from their vehicles, greatly improving both convenience and efficiency. Target is advancing this idea by testing a combination of Starbucks orders with curbside returns at certain Minneapolis locations, offering a streamlined return process alongside the bonus of picking up a Starbucks order. Furthermore, these retailers are enhancing the experience with added features such as notifications through mobile apps and allocated parking spots for even smoother curbside returns, showcasing their dedication to elevating customer satisfaction and building loyalty.

Takeaways

In summary, return collection strategies, as illustrated, mainly provide early-stage reverse logistics benefits and some cost reductions for retailers. Yet, these benefits are slight in comparison to the potential for lost sales and the environmental concern of high-quality items being discarded and going to landfills- which sometimes is unfavorably determined by computer algorithms at the return center despite the items’ high quality and sustainable future lifecycle. This issue is particularly pertinent given the shift in consumer behavior among younger generations, such as Gen Z and Millennials, who show a growing preference for buying second-hand items, bolstered by the popularity of resale platforms like Poshmark and ThredUp.

I believe there are significant opportunities for entrepreneurs in this industry to leverage Teixeira’s Decoupling Theory to pursue innovative business models. These new business models should differ from traditional ones by reconfiguring the value chain. Steps like the costly operation of inspection and grading could be shifted earlier in the process, incentivizing returners to perform these tasks for brands. Additionally, insights from Christensen’s Disruptive Innovation Theory highlight possibilities for creating new markets out of non-consumption market segments, particularly aiding smaller brands facing low ROR (Rate of Recovery) and less attractive options like bulk liquidations to build out their own branded secondary market to connect to new wave of discount buyers directly.

The key challenge lies in aligning current reverse logistics operations with the demand for high-quality, reusable items quickly and economically, matching the ever-increasing supply of returned/unwanted items to the end-users who are the highest bidders. The last word is despite the linear progress in improving the efficiency of return collection, the billion-dollar challenge of predictable resale is still the most significant hurdle and an unaddressed opportunity for return industry transformation, which I plan to explore further in the last two chapters.

The industry faces a critical billion-dollar challenge: efficiently and predictably reselling returned or unwanted items on a large scale to end-users ready to pay the highest price. This pivotal issue demands inventive solutions that simultaneously address consumer convenience and retailer cost-efficiency, shaping the future of the marketplace.

State of Union for Return Resale: The most vital and underinvested step in return landscape

Previously, I explored the initial stages of the return process, focusing on collection and inbound logistics as outlined in Chart 7. Now, I turn my attention to Steps 4 and 5 from the same chart, examining the reselling dynamics and the state of the secondary market.

The rise of E-commerce and a corresponding increase in customer returns have significantly propelled the growth of Secondary Market Liquidation and Re-commerce business models. As we navigate through the lifecycle of E-commerce products — from their launch in the primary market to their transition into secondary markets — we encounter a range of evolving trends. This journey not only looks at how consumers initiate returns but also at their engagement with used or second-hand items. Chart 10 offers a comprehensive snapshot of this ecosystem, highlighting both traditional and innovative approaches to resale and liquidation.

Consumer return liquidation plays a pivotal role when major retailers and brands outsource the handling of billions of dollars in unwanted and returned inventory to third-party wholesale liquidation firms. These companies operate either independent or branded resale B2B marketplaces, where they supply large quantities of graded returned inventory to thousands of business buyers, typically through auctions or significant discounts [as depicted in the left section of Chart 10]. Although the recovery rates for these sales are generally low, these organizations are highly efficient at facilitating the liquidation process.

Despite offering less favorable economics on a per-unit basis for brands (with recovery often ranging from 5–8 cents on the dollar), this method has been the go-to strategy for decades, particularly for large online and brick-and-mortar retailers such as Wayfair, Walmart, Home Depot, Amazon, and Costco. These entities prioritize quickly clearing returned goods from their storage facilities or return centers, many of which are managed by B2B liquidation specialists like Bstock.com.

Typically, these liquidation marketplaces offer various revenue models, including consignment-based, revenue-share, or full-purchase options. Key players in this industry encompass Liquidation.com, Bulq.com, Bstock.com, directliquidation.com, quicklotz.com, viatrading.com, and 888lots.com. Chart 11 represents the competitive landscape within the secondary market B2B liquidation industry as of Sep 2023, including monthly traffic data (as a proxy for market share).

Conversely, the market for second-hand and used products, especially in clothing and fast fashion, has seen significant growth in recent years. This movement, often described as re-commerce or the circular economy, has become increasingly popular among Gen Z and Millennials, who are moving towards sustainable fashion choices. These younger consumers show a marked preference for buying pre-owned and pre-loved clothing, fueling a rapid expansion of re-commerce platforms and two-sided platforms that connect sellers with buyers like never before. While many of these platforms are still on the path to profitability (for instance, ThredUp achieved its first quarterly adjusted EBITDA breakeven in Q3, 2023 after several years as a public company), their growth potential is unmistakable.

Gen Z, in particular, is expected to catalyze a boom in the resale sector. According to ThredUp, the U.S. resale market is forecasted to hit $70 billion by 2027, with Gen Z at the forefront of this surge. This generation’s preference for thrifted and second-hand purchases is not only transforming the fashion industry but is also predicted to push the second-hand clothing market beyond the scale of fast fashion by 2030. This indicates a profound shift in consumer behavior and the overall fashion ecosystem. Chart 12 summarizes traffic data and serves as an indicator of market share among leading clothing resale and re-commerce platforms as of September 2023.

The emergence of new tech enablers like Archive, Recurate, Reflaunt, and Treet marks a significant shift in the retail landscape, particularly in the secondary market domain facilitating trended brand-owned peer-to-peer resale programs. These white-label resale solutions empower brands to establish secondary market store websites, taking back control of their brand equity and customer experience by allowing consumers to sell used items directly to other peers on the brands’ websites- rather than relying on external platforms like ThredUp, Depop, or Poshmark to handle their products’ resale, brands can now manage the resale process in-house. This model fosters a sense of community among brand loyalists and ensures that products circulate within the brand’s ecosystem, enhancing sustainability and customer engagement.

Trove.com stands out as a significant contributor to this sector, adopting a more involved approach than Archive and Recurate’s focus on peer-to-peer exchanges and white-label solutions. Trove collaborates with brands such as Patagonia and Lululemon, overseeing the logistics involved in collecting, refurbishing, and reselling used items through the brands’ re-commerce sites, like https://likenew.lululemon.com/ or https://wornwear.patagonia.com/. This method adds a layer of quality control and convenience, further bridging the gap between traditional retail and the burgeoning e-commerce market

Brands have immense trust and experience that third-party marketplaces can’t match. There is no replacement for buying Patagonia at Patagonia or Lululemon from Lululemon. It is similar to the experience of buying a certified pre-owned Lexus directly from Lexus rather than from a used car lot. (Andy Ruben, founder of Trove)

Takeaways

In recent years, a distinct divergence has become apparent between the booming market for second-hand or “pre-loved” goods and the somewhat stagnant area of returns and surplus items. Chart 10 vividly illustrates this divide; the right side showcases significant progress and innovation within the second-hand goods ecosystem, while the left side, focuses on returns and excess stock — a market ballooning to a value of over $816.8 billion as per Chart 2 — shows a notable lack of groundbreaking innovations or business models aimed at enabling brands to resell these items efficiently, with minimized costs and maximized returns.

An important insight from Chart 4 is that a large fraction of returned goods, around 80%–85%, are not defective and could feasibly be reintroduced into the secondary market. Yet, there’s a stark difference in ownership and motivation between the second-hand market and the returns landscape. In the former, the consumer owns the product, providing a clear motivation to resell items that are no longer needed, in exchange for cash or credit towards future purchases. This ownership creates a direct incentive for active participation in the resale market. On the other hand, in the context of retail/E-commerce returns, the items technically remain the property of the brands, with consumers primarily focused on securing refunds. This setup leads to limited consumer engagement in the resale process, presenting a substantial hurdle for brands looking to repurpose these items effectively.

Chart 7 outlines the intricate process and associated costs of preparing returned items for resale, including the logistics of returns, issuing refunds, and the brand’s role in either reselling or liquidating the product. A significant challenge, as indicated in Chart 7, lies in the logistical costs tied to returns, prompting brands to opt for quick, cost-effective solutions that often overlook more sustainable or profitable alternatives. This preference for immediate cost reduction over exploring sustainable and profitable avenues stands as a major impediment to innovation within the returns sector of E-commerce.

New Wave of Disruptive and Business Model Innovation

As a student of disruptive innovation theory, inspired by the work of Clay Christensen and business model innovation via the decoupling theory (developed by Thales S. Teixeira and Greg Piechota), which customers drive, I am constantly exploring opportunities within the realm of return management, re-commence, and reverse logistics businesses. I aim to explore new solutions that can enhance the economics of e-commerce return units, leading to new business model innovation driven by changes in consumer behavior.

The new technology isn’t driving most disruption today. Consumers are disrupting markets (Thales S. Teixeira,“Unlocking the Customer Value Chain”)

The decoupling theory is among the most intuitive and robust constructs that can uncover the business model innovation by breaking off and decoupling the weak links between different customer activities traditionally glued together and provided by one company. To zoom in, Chart 13 summarizes all key activities owned by other consumers (returners), brands, or partners in the E-commerce Return Value Chain.

According to the decoupling framework, there are three types of activities that future entrepreneurs can tackle to decouple and create more values and disrupt the return landscape via business model innovation:

- Value Creation: This involves activities that directly generate value for customers, such as selling a product (like a car or a meal) or initiating a return process for a refund. These actions enhance the customer experience and satisfaction by offering tangible benefits or services.

- Value Charging: These are activities where a charge is applied for the value provided, for example, a commission on a car sale, a fee for a meal, or costs associated with processing returns, including inbound shipping and reverse logistics. This step is crucial for monetizing the value created.

- Value Eroding: Activities falling under this category do not contribute to creating or charging for value. Examples include the effort involved in listing a used car for sale, traveling to pick up a meal, or the customer’s time spent preparing items for return. These actions often represent a loss of time or resources without direct compensation or value enhancement.

In the discussions of recent sections, there has been a notable focus on enhancing efficiency and reducing the costs tied to return collections for brands. Innovations like Happyreturns’ hub and spoke model, which aggregates returned items, and doorstep pickup services, which improve customer convenience, are steps toward reimagining the E-commerce Return Value Chain. These efforts aim to decouple activities that erode value or involve charging customers and brands, addressing critical inefficiencies. However, while these innovations in managing return collections — aimed at streamlining and reducing the costs associated with return logistics — may offer some cost savings, the impact remains relatively modest. For instance, tackling transportation and inbound shipping costs might reduce expenses by up to $6, a small portion of the total return costs, which can represent up to 66% of a $50 item’s price. This highlights the need for more profound business model innovations to significantly mitigate the financial burden of returns.

In my perspective, a significant hurdle remains in swiftly and efficiently reselling returned items to the most appropriate end-users (those with the highest willingness to pay) at scale. This issue has been largely neglected by recent business model innovations owing to its fragmented landscape and the intricate, multifaceted cost structures involved.

Exploring Opportunities to Enhance Return Unit Economics

Our examination of reselling tactics such as bulk B2B and B2B liquidations in the “State of the Union for Return Resale” segment reveals that these approaches generally favor large retailers dealing with high volumes of returns, where the speed of return processing often takes precedence over maximizing recovery value. Consequently, these retailers are able to work effectively with leading wholesale liquidators (like Liquidity Services, B-Stock) despite low recovery rates. However, for small to mid-sized brands, especially those in the high-return sectors like apparel, recovering minimal amounts per dollar from returns is not sustainable, as return rates can soar up to 26% (Shopify data).

This raises a critical question of what the next wave of business model innovation could offer, possibly by applying decoupling theory (across different activities depicted in Chart 13) or exploring the entire return management process through the lens of Clay Christensen’s disruptive innovation. This could potentially enhance return unit economics for smaller brands beyond merely collecting returns. Specifically, is it possible to disrupt the return management domain with solutions that are both cost-effective and efficient, catering to smaller brands with fewer resources? Moreover, how can we serve non-consumer brands that currently have no option but to default to landfill disposal for returns?

Predicting the future and direction of the return management ecosystem is challenging, especially with the advent of Generative AI in recent years, opening up possibilities for novel experiences. Nevertheless, I propose to outline three key opportunities within the e-commerce return value chain where brands could significantly improve their return economics. Chart 14 provides a high-level summary of these three areas. Each area warrants a detailed discussion, which I plan to explore in future articles. For now, let’s envision a feasible future for the next wave of business model innovation, which could be driven by:

a) Shifts in consumer behavior both before purchase in the primary market and after returns, at the stage of reselling items to the new wave of end-users.

b) The strategic decoupling and recoupling of certain value-eroding and value-charging activities within reverse logistics, offering brands a chance to substantially lower reverse logistics costs.

The Rise of Generative AI in driving new business model innovations in E-commerce Return space

The rise of AI-first marketplaces promises a transformative era in the e-commerce and returns logistics landscape, as detailed in Pete Flint’s NFX article on “The AI-First Marketplace.” This evolution is driven by generative AI’s unparalleled capabilities to reimagine and vastly improve unit economics and customer experiences. Key innovations empowered by AI, particularly in managing e-commerce returns, showcase how this technology acts as a crucial facilitator and lubricant, making previously inconceivable solutions possible and efficient, fast, and scalable. I mentioned a few of them in Chart 14, but below are the ones that I think we are closer to implementing amd can address both brand and consumer needs more effectively than ever before.

- AI-Enabled Pre-Sale and Product Bundling: AI now enables marketplaces to anticipate returns, crafting personalized video emails that detail product features and reasons for returns, offering them at a discount before they’re even returned. This not only addresses inventory challenges preemptively but also showcases AI’s potential in merging predictive analytics with customer interaction.

- Intelligent Return Management: AI chatbots have evolved into sophisticated platforms that engage customers directly, understanding their reasons for returns and guiding them through self-inspection. This enhances the customer experience and feeds valuable data back into the system, streamlining the return process.

- Enhanced Search and Matching Capabilities: Generative AI significantly improves marketplace efficiency by enhancing search algorithms and facilitating better matches between returned products and potential buyers. By analyzing extensive data sets to understand consumer preferences, AI enables marketplaces to tailor product recommendations and bundle returns, driving sales and minimizing the economic impact of returns.

Final Reflections: A Vision for the Future of E-commerce Returns

As we circle back to all discussions, it’s evident that the realm of e-commerce returns is ripe for transformative solutions, including the advent of AI-first marketplaces, aimed at redefining the liquidation landscape. Such innovations promise brands more economically viable strategies for navigating the often unpredictable world of product returns, moving away from the conventional, linear methods that currently predominate.

Today’s standard practices for managing e-commerce returns fail to effectively tackle the intricate, non-linear intricacies of the return process. Caught in an existing value chain and compensation framework, e-commerce consumers witness little emphasis on sustainability or efficiency. Consequently, brands, which are the central figures in this equation, incur financial losses without making substantial contributions toward environmental sustainability.

The responsibility rests with a new wave of entrepreneurs to create groundbreaking business models that improve the return process from start to finish, beyond merely facilitating the inbound shipping and return collection. This approach seeks active engagement from both brands and consumers (returners) within this dynamic environment. In the discussions to follow, I aim to explore a variety of concepts, with two particularly exciting prospects at the forefront:

- Utilizing Generative AI: The application of generative AI can generate heightened demand for returned items, which frequently retain a high level of quality (on average, 80%). Whether through individual products or specially curated customer packages, this strategy, marketed in advance, promises faster sales and enhanced recovery rates.

- Adopting Brand-Centric Circular Economy and Resale Initiatives: As the movement towards brand-centric circular economies and resale efforts gains momentum, powered by tech solutions like Archive.com, Trove, and Recurate, an increasing number of brands are motivated to create their secondary markets, moving away from third-party platforms. This evolution enables brands to leverage their established market presence and customer base to swiftly align returned items with new purchasers, thereby expediting the resale process and optimizing returns.

I remain hopeful that we’ll witness significant progress in these domains shortly, introducing more sustainable and financially sound practices for managing e-commerce returns. Such advancements promise to enrich the social and financial value for all stakeholders involved in the e-commerce returns ecosystem.